[ad_1]

During a period when long-term interest rates are rising quickly, you will see headlines that bonds are performing poorly, because their market values must decline as interest rates go up. But long-term investors who hold bonds for income may have a different opinion: If bond issuers are making their interest payments, the bonds are performing well. Still, it isn’t fun to watch your market value and your portfolio balance decline.

MarketWatch readers reacted in droves to Aarthi Swaminathan’s coverage of the mortgage-lending market. She interviewed economists who believe U.S. mortgage loan rates might climb to 8%, which no longer seems to be a stretch, with Freddie Mac saying the national average rate for a 30-year loan was 7.09% as of Thursday. For 15-year mortgage loans, the average rate was 6.56%, according to Freddie.

Vivien Lou Chen looks into the reasons why the yield on 10-year U.S. Treasury notes jumped to 4.31% on Thursday, the highest level since November 2007, while also explaining how the Treasury Inflation Protected Securities (TIPS) market shows how much higher investors expect the “real” cost of borrowing — interest rates minus the inflation rate — to get.

One factor sending bond prices lower — and rates higher — was the release on Wednesday of the minutes of the Federal Open Market Committee’s July 25-26 meeting. Most participants in the Fed policy meeting “continue to see significant upside risks to inflation, which could require further tightening of monetary policy,” according to the minutes.

Market Extra: How higher-for-longer rates are playing out as 10-year yield hits 15-year high

Early on Friday, the yield on 10-year Treasury notes

BX:TMUBMUSD10Y

declined to 4.22%.

Joy Wilthermuth interviews Ryan Murphy, director of fixed-income business development at Capital Group, who explains why bond investors should wait while getting paid their interest and “know this is going to work out in the end.”

From the daily Need to Know column: Bond yields hold the key to an emotional market that can change on a dime, says this strategist

A gloomy look ahead to 2025: Risky bonds are facing a ‘maturity wall’ that could sow more panic in markets

Housing market evolves

With homeowners reluctant to sell their homes and give up their existing low mortgage rates, the demand for new homes has spiked.

Scott Olson/Getty Images

With mortgage loan rates at their highest level in 21 years, homeowners are reluctant to sell if they locked in low interest rates before March 2022, so builders have been ramping up construction of new homes.

Here’s more coverage of the housing and mortgage lending markets from Aarthi Swaminathan:

How bond funds navigate the turbulence

MarketWatch illustration/iStockphoto

For this week’s ETF Wrap, Christine Idzelis interviews Rick Rieder, the chief investment officer of global fixed income at BlackRock, who talks about the firm’s strategies for its actively managed exchange-traded bond funds.

Sam Reid co-manages the River Canyon Total Return Bond Fund RCTIX, which is rated five stars, the highest rating, by Morningstar. He explains how the fund makes use of credit-investing strategies employed by hedge funds managed by the same firm.

From recession fear to ‘soft landing’ to ‘no landing’

Federal Reserve Chair Jerome Powell may need to take a subdued approach to fighting inflation during the election cycle.

Alex Wong/Getty Images

The annual U.S. inflation rate was 3.2% in July, which is well above the Federal Reserve’s long-term target of 2%. But inflation has come down enough for economists to change their tune, going from predictions that a recession would result from the Fed’s cycle of interest-rate increases that began in March 2022, to talking about a “soft landing” scenario, with the Fed succeeding in tamping down inflation with only a mild recession resulting, to a buzzy new “no landing” scenario, in which the U.S. economy keeps chugging along with inflation remaining elevated. That may be the worst of the three scenarios for the stock market.

Greg Robb looks into a complicated set of scenarios and possible decisions for the Fed, including the ramifications for the 2024 election cycle.

Dividend stocks

Getty Images/iStockphoto

Michael Brush makes the case for buying stocks with high dividend yields right now, in part because a large portion of long-term returns for investors has come from the payouts.

Another approach to dividend stocks is to hold them long term to build income streams over time. This means the initial dividend yields may not be very high. Here are 20 dividend stocks that have been the best income growers in the S&P 500 over the past five years, among those that began with dividend yields of at least 1.5%.

China’s trillion-dollar problem

The almost-daily news flow out of China as large property developers default on bond payments signals the need for the country’s government to step up with a $1 trillion rescue plan, according to Marko Papic, the chief strategist at Clocktower Group, who spoke with Joy Wiltermuth.

But Isabel Wang spoke with economists who dig into a complicated set of reasons that investors shouldn’t count on China’s government to come up with a massive stimulus package.

More worries: Why U.S. stock-market investors need to keep an eye on a weak Japanese yen

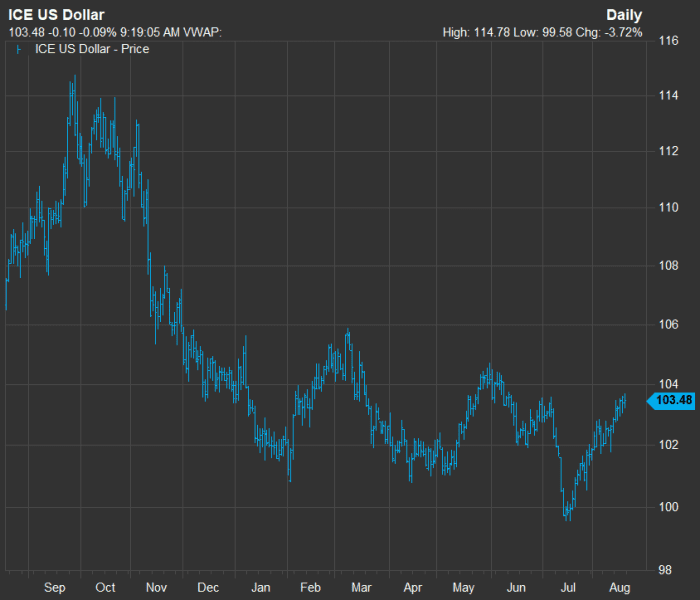

Dollar roars back

The ICE U.S. Dollar Index was up 4% early on Aug. 18 from its July low.

FactSet

After hitting a 20-year record in September, the ICE U.S. Dollar Index

DXY

fell to a low in July before taking a 4% upward swing. Joseph Adinolfi reviews factors leading to the dollar’s rise and looks ahead at possible implications.

More from Joseph Adinolfi: Same bank, two different stock-market calls. Why internal disagreements rage on Wall Street.

Retail ‘shrink’ and a price comparison

Scott Olson/Getty Images

Retailers had mixed news for investors this week, as usual, but there was also a lot of attention on shoplifting and other causes of inventory “shrink.”

First, the earnings news and corporate outlooks:

James Rogers reports on retailers comments’ about theft and inventory shrink in general:

-

Walmart Inc.

WMT,

+1.44%

CEO Doug McMillon indicated that shoplifting varies by region. -

Target Corp.

TGT,

+0.85%

CEO Brian Cornell said the company was facing an “unacceptable amount” of theft, with some attributed to organized crime. -

Executives at Home Depot Inc.

HD,

+0.03%

are hoping a new federal law will help curb shoplifting.

In the Financial Faceoff column, Leslie Albrecht compares prices for school supplies at Walmart and Target.

Advice from the Tax Guy

Andrew Keshner — the Tax Guy — has advice for a reader who, along with two siblings, inherited a house six years ago. One sibling wants to keep the house and the other two don’t, but all three want to limit their tax burdens. Here are various scenarios for them to consider.

Keshner also reports on the Internal Revenue Service’s new efforts to catch people who cheat on their taxes.

Taking off his tax hat, Keshner looks at the results of a study on consumer behavior that concludes that people are spending a lot of money on subscription services they don’t even use. A self-audit can save you a lot of money.

Uber and the changing city

andrew caballero-reynolds/Agence France-Presse/Getty Images

Uber Technologies Inc.

UBER,

has changed many urban landscapes. We have gone from being unable to hail a taxicab in Midtown Manhattan 10 years ago to having at least three compete for your business if you raise your hand for service while standing outside the News Corp.

NWSA,

building on Sixth Avenue. Uber’s easy ride-hailing service has made a complete change to this aspect of city life.

But not everyone is happy with Uber. For the Book Watch column, Levi Sumagaysay interviews Kafui Attoh and Katie Wells, two of the authors of “Disrupting D.C.: The Rise of Uber and the Fall of the City.” They describe how Uber has managed to change so many cities, how difficult it can be to work for the company and why it is still a compelling option for its drivers.

Want more from MarketWatch? Sign up for this and other newsletters to get the latest news and advice on personal finance and investing.

[ad_2]

Source link