[ad_1]

After a catastrophic year, bonds in 2023 are showing signs of promise, with investors eyeing higher yields and falling U.S. inflation as potential reasons to explore their options in the $53 trillion debt market.

It’s no secret that bond returns were one of the biggest casualties last year of the Federal Reserve’s rapid pace of interest rate hikes, which triggered a historic rout across financial markets and left the S&P 500

SPX,

with its worst year since 2008.

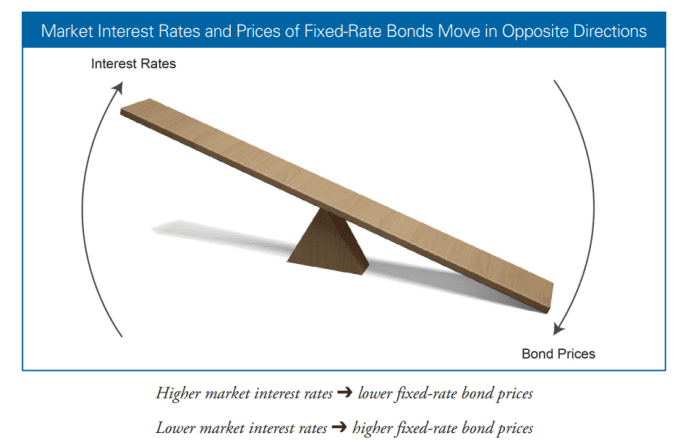

The classic “60/40” portfolio, dedicated mostly to stocks plus a smaller share to bonds, failed to soften the blow for investors when equities and debt both plunged in value, because when interest rates rise, bond prices fall.

Interest rates and bond prices move in the opposite direction

U.S. Securities and Exchange Commission’s Office of Investor Education and Advocacy

Now, with the Fed potentially nearing a point where interest rates could soon peak, fixed-income professionals have been fielding a torrent of questions around the same theme: Should investors once bitten, be twice shy about bonds?

“The simple answer is that bonds, as an asset class, simply have not been this compelling in 15 years,” said Daniela Mardarovici, co-head of multisector fixed income at Macquarie Asset Management.

“All of the features we used to talk about when it comes to bonds, like income, stability and as a counterbalance to a recession, this year, bonds once again have those features.”

How bonds work

Like a loan, bonds are a contractual obligation to pay back debt over time. The terms spell out how much is due each year in principal and interest, until the bond matures.

The first thing potential investors should focus on for 2023 is the higher starting yields of bonds, whether it’s someone considering allocating more of a 401(k) to fixed income, a retiree researching a bond mutual fund or a person looking to buy securities directly from the U.S. Treasury.

“Before the pandemic, you’d be struggling to get 2% to 4%,” Mardarovici said. “Now 5% to 6% is easy, and you don’t have to look under the darkest rock to find it.”

After an era of low interest rates, it helps that the “risk-free” 2-year Treasury yield

TMUBMUSD02Y,

has climbed back above 4.2%, up from a one-year low of about 1.2% in February. The 6-month rate

TMUBMUSD06M,

on Tuesday also was near 4.8%, according to FactSet.

“When looking at long-term returns, the biggest predictor in bonds is the starting yield,” Mardarovici said.

Bonds that carry credit risk pay investors a spread, or premium, above the Treasury yield, which can borrowing costs higher. The U.S. government isn’t deemed a default risk even though the Treasury Department in January began taking “extraordinary measures” to keep the federal government current on its bills, while giving Congress more time to increase or suspend the debt ceiling.

Billions flow into bonds in January

Last year was an ugly reminder of how inflation and rising interest rates can be kryptonite for bonds, particularly when the U.S. market mushroomed in a low rate world.

The Fed’s rapid pace of rate hikes since March last year now point to headway in its fight to pull inflation lower. The U.S. consumer-price index rose at an annual rate of 6.5% in December, down from a peak of 9.1% in June, but still was far above the Fed’s 2% target.

“We are approaching peak rates by the Fed and inflation is falling,” said Maria Vassalou, co-chief investment officer of multiasset solutions at Goldman Sachs Asset Management. “At this point, bonds can be both a source of real return, but they can also act as a hedge against positions in risky assets.”

Other investors appear to be adopting a similar line of thinking. In the year’s first four weeks, flows into funds dedicated to less risky investment-grade bonds totaled $9.1 billion, or about 2.4% of their assets under management to start the year, analysts at Goldman Sachs said in a weekly client note.

“From a flow perspective, the picture has improved dramatically,” said Brendan Murphy, head of core fixed-income, North America at Insight Investment.

Returns also have bumped higher. Using the Barclays Bloomberg U.S. Aggregate index as a proxy for the broader U.S. bond market, returns were up about 2.7% to kick off the year, according to FactSet data, which still showed a negative 8.7% return for the index from a year ago.

Bond risks

While 2022 may have been as bad as it gets in terms of deeply negative total bond returns, today’s higher yields can provide a portfolio with some downside cover.

Still, there could be two key ways for bond investors to get hurt, Murphy said, including if economic growth slows and riskier company defaults pick up, or if bond investors have it wrong and inflation hasn’t yet peaked.

“It may be off the peak, but what if it doesn’t get back down to a 2% rate,” he said, noting that in such a scenario the Fed could be forced to increase its policy interest rate above its roughly 5% peak target.

But right now, those two risks don’t look like too big of a threats Murphy said. Although, he thinks they could rear up in the next year or two.

[ad_2]

Source link