[ad_1]

Gold, XAU/USD, US Dollar, Powell, FOMC, Fed, Treasury Yields, US CPI – Talking Points

- Gold is bumping along recent lows with the US Dollar looking for direction

- Market priced inflation readings are pondering lower energy prices against high services costs

- Fed Chair Powell will be speaking later today. Will his comments hit XAU/USD?

Recommended by Daniel McCarthy

How to Trade Gold

The gold price is languishing around 3-month lows going into the Wednesday session ahead of Federal Reserve Jerome Powell speaking later today.

The Fed boss will appear at the European Central Bank (ECB) Forum on Central Banking in a policy panel discussion in Sintra, Portugal.

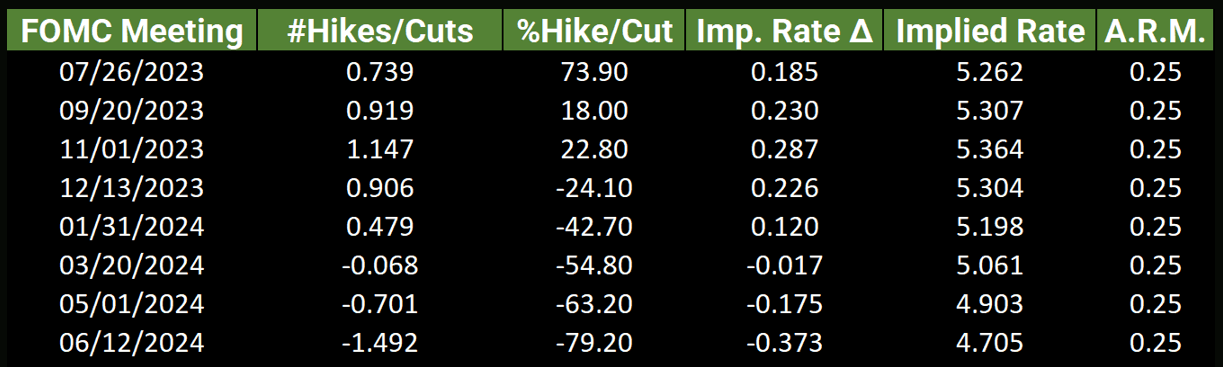

Last week he reiterated the banks tightening bias after its pause in rate hikes at the June Federal Open Market Committee (FOMC) meeting. The so called ‘hawkish hold’ led markets to hope for a potential rate cut in the foreseeable future.

Such notions have been dashed and rates markets are now looking at early 2024 as the earliest time horizon for an easing in monetary policy.

Source; Bloomberg, tastylive

The recalibration of the perception for the Fed’s rate path saw the US Dollar notch up some notable gains going into the end of last week, but this week has seen more range trading/sideway price action in many currency pairs.

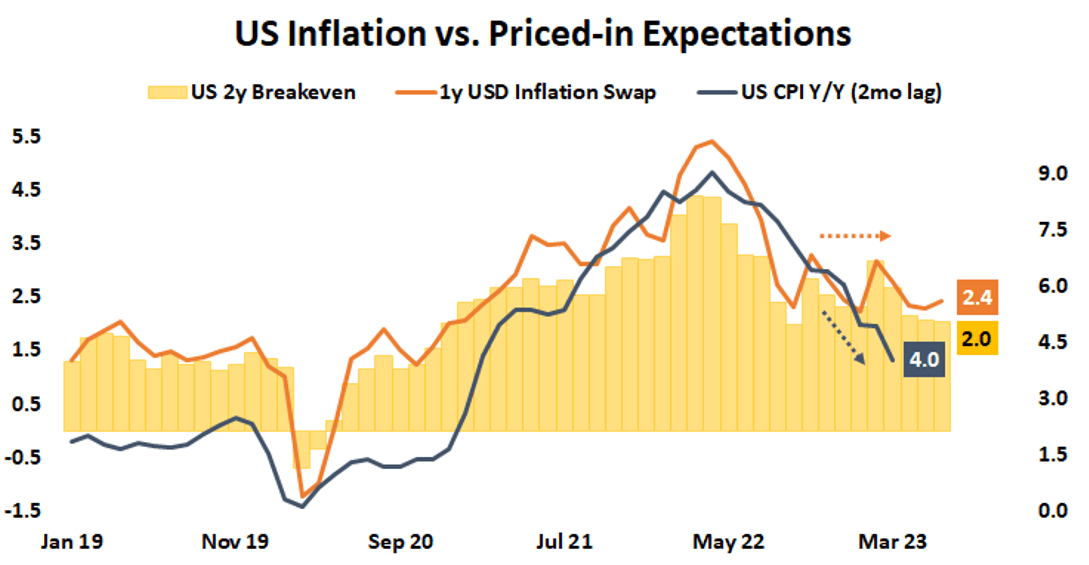

This comes as inflation expectations have reaccelerated a touch with the 1-year US Dollar inflation swap ticking slightly higher recently.

The 2-year breakeven inflation rate has also flattened after a period of easing in the first part of 2023. The breakeven inflation rate is the market-priced inflation rate derived from Treasury inflation-protected securities (TIPS).

Source; Bloomberg, tastylive

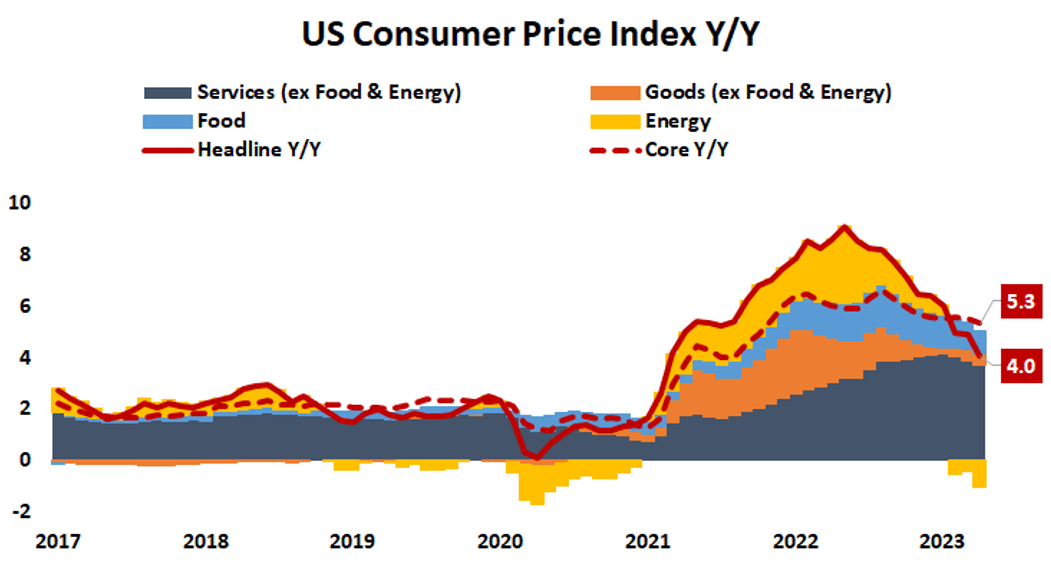

A potential source of reasoning for the market recognition that inflation could be sticky going forward may lie in the breakdown of CPI.

In particular, looking closely at the impact of energy prices within the headline inflation gauge, this is where the Fed might have concern as well as the swap market.

Recommended by Daniel McCarthy

Introduction to Forex News Trading

Source; Bloomberg, tastylive

Russia have been flooding available markets with oil exports in order to fund the conflict within the Ukraine. It has been reported this week that Russia overtook Saudi Arabia as China’s number one supplier of energy.

Headline US CPI has been tracking lower, but this might be short lived once the impact of lower energy prices is taken into account.

The Fed have cited the robust price pressures that remain within the services sector and this part of the economy appears to remain tight with a resilient labour market in the face of tightening policy.

US CPI data on the 12th July will be watched closely for clues on the Fed’s posture going into the July 26th FOMC gathering.

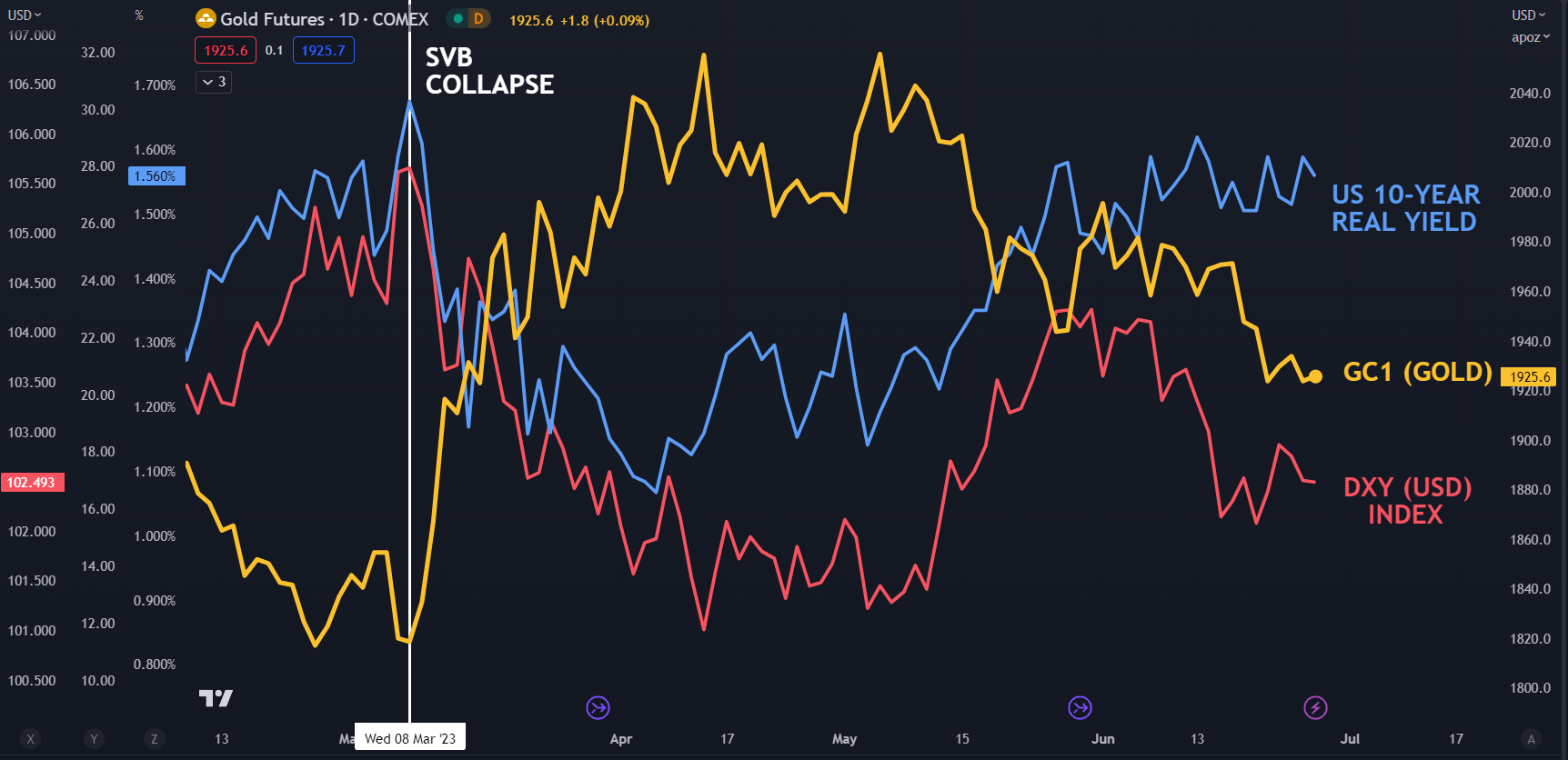

For the gold price, a key component out of the inflation outlook could be the ramifications for US real yields. The real yield is the nominal yield less the market-priced inflation rate derived from Treasury inflation-protected securities (TIPS) for the same tenor.

This has the potential to be a two-edged sword for the precious metal. If CPI tracks higher again, it could force the Fed into a more aggressive tightening stance which may initially be supportive for the US Dollar.

However, it may lead to higher inflation expectations, that might see real yields dip, making the yellow metal a potentially attractive asset.

The key for such an outcome will be the reaction in Treasury yields. If they were to lift above the increase in market priced inflation, real yields could inch higher, possibly undermining the gold price.

GC1 (GOLD FRONT FUTURES CONTRACT) AGAINST US 10-YEAR REAL YIELD AND DXY (USD) INDEX

— Written by Daniel McCarthy, Strategist for DailyFX.com

Please contact Daniel via @DanMcCathyFX on Twitter

[ad_2]

Source link