[ad_1]

Our call of the day, from LPL Financial’s asset allocation strategist Barry Gilbert, says it’s time to reconsider a beaten-down, but once-popular investment strategy.

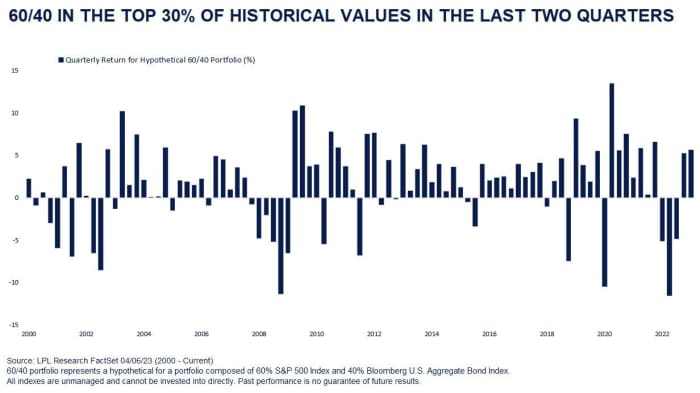

“There deservedly was a lot of hand-wringing about the death of the 60/40 portfolio in 2022, a portfolio of 60% stocks and 40% bonds,” Gilbert wrote in a note. “What was most surprising for the 60/40 in 2022, of course, was how spectacularly bonds failed to play their traditional role as a portfolio diversifier in a down market for equities.”

While investors are used to choppy paths to longer-term stock gains, he said they were stunned by bond volatility, of which 2022 delivered plenty. But things are starting to look brighter for the 60/40, he said.

“While the fourth quarter of 2022 and the first quarter of 2023 weren’t spectacular for the 60/40, using the total return for the S&P 500 index and the Bloomberg U.S. Aggregate Bond Index as our proxy for stocks and bonds, the 60/40 has been on solid footing the last two quarters, as seen in the chart below,” said Gilbert.

Looking ahead, he says investors can find even more reasons to reconsider the strategy.

“Looking at bonds from a tactical perspective, with higher starting yields, a Federal Reserve likely near the end of its rate hiking campaign, and inflation coming back down, not only do return prospects look brighter for bonds, we believe they have become more likely to return to their historical role of a portfolio diversifier in the event of an economic downturn,” said Gilbert.

On the equity side, he admits there is more uncertainty given Fed policy tends to act with a lag, but is also not anticipating a steeper downturn and doesn’t think markets will overreact to a modest one.

On a strategic time frame, LPL’s long-term stock and bond forecasts, based on the S&P 500 and the Bloomberg Aggregate as proxies, indicate improvement from last year to 2023. Stock valuations are still a bit elevated based on history, but did improve in the pullback, while the jump in bond returns “is even more meaningful as the downside from higher yields turns into upside looking forward,” he said.

Gilbert says wary investors, understandably, may still not be ready to fully embrace the 60/40, especially given caution on fixed-income markets in particular.

“There were also some effective hedges against losses in 2022 that investors can sometimes forget when the 60/40 is on a roll, especially in alternative investments. We do believe that there are ways in which a portfolio can be better diversified beyond the traditional 60/40, but we think the 60/40 remains a sound foundation for a diversified portfolio, both tactically and strategically, something that is easy to forget after the challenges of 2022,” he said.

Read: ‘Sell the last hike’ was the best stock strategy in the inflationary 70s/80s, says BofA

Best of the web

Cities want offices turned into homes. This is what a key NYC developer says is being ignored.

Two U.S. lawmakers reportedly traded in bank stocks last month as they worked to address fallout over a recent crisis in the sector.

Random reads

The Met Gala, aka Karl Lagerfeld’s literal cat walk

“P 7” — the $15 million license plate.

And introducing Fedha, Kuwait’s new AI news anchor.

Need to Know starts early and is updated until the opening bell, but sign up here to get it delivered once to your email box. The emailed version will be sent out at about 7:30 a.m. Eastern.

Listen to the Best New Ideas in Money podcast with MarketWatch reporter Charles Passy and economist Stephanie Kelton

[ad_2]

Source link