[ad_1]

It’s too early to know which sector will lead U.S. stocks higher in the next bull market. But it’s not too early to have confidence that what it won’t be is the energy sector.

Energy has been the best performer during this bear market. At no time over the last 5+ decades has the same sector been at the top of the sector rankings in a given bear market and in the subsequent bull market as well.

I reached these and other conclusions upon analyzing the S&P 500’s

SPX,

sector rankings in each bull and bear market since the early 1970s, courtesy of data compiled by Ned Davis Research. According to the firm’s bull and bear market calendar, since then there have been 14 complete bull markets and 14 complete bear markets.

I found that, on average among the 10 S&P 500 sectors, the first-place winner in a given bear market’s ranking was in 9th place for performance in the subsequent bull market. Conversely, the sector ranked in 10th place (last) in a given bear market was in 4th place for performance in the subsequent bull market.

What if you look back to the prior bull market as opposed to the immediately prior bear market? A similar picture emerges: On average, the sector at the top of a given bull market’s ranking drops to 5th place (out of 10) in the subsequent bull market. The sector at the bottom of a given bull market’s ranking climbs to 7th place, on average, in the subsequent bull market.

The bottom line: The best guess is that the sector that will lead the next bull market is higher has not been at the top of recent rankings.

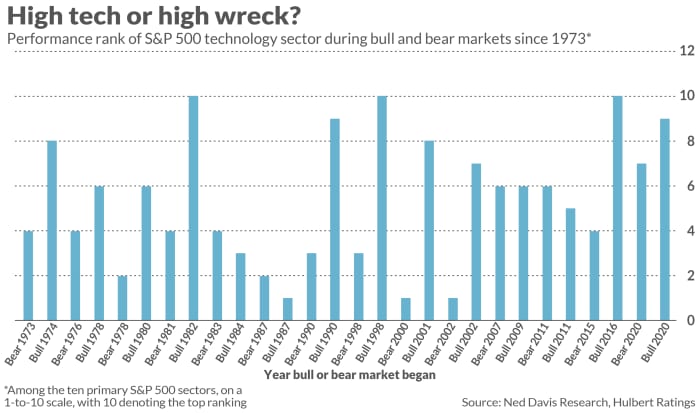

Got tech?

Speculation about the next bull-market leader is especially intense when it comes to the technology sector. While a stellar performer during the bull market that began at the March 2020 bottom, tech has suffered mightily in this bear market.

Enthusiasts are hoping that the sector will bounce back to the top of the sector rankings in the next bull market. I wouldn’t bet on it. Since the early 1970s, there has been just one instance in which the same S&P 500 sector topped the rankings in two successive bull markets. These were the ones that began in February 1978 and April 1980, and the top sector in each was Industrials.

Moreover, the Information Technology sector’s ranking across the various market cycles has been especially volatile.

This isn’t to say that technology stocks will be mediocre (or worse) performers in the next bull market. Technology has evolved enormously since the 1970s, as has its role in the economy. So it’s possible that the world has changed enough that “this time will be different.” But those arguing now that it will be different have already stopped looking at history anyway.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at mark@hulbertratings.com

[ad_2]

Source link