[ad_1]

S&P 500, US Dollar, Crude Oil, Natural Gas, Gold, NZD, AUD, CAD, Fed – Talking Points

- The S&P 500 is unchanged in Asia as it nervously awaits Powell’s speech

- APAC equities have been lifted by positive regulatory hopes while crude dipped

- All eyes on Jackson Hole today.What is the weight of words worth for the S&P 500?

The S&P 500 held onto overnight gains ahead of the much-anticipated address by Federal Reserve Chair Jerome Powell later today.

The Dow Jones and Nasdaq also finished up on the day. Higher stock prices and narrowing corporate bond spreads are signs of easing of monetary conditions.

This is the opposite of what the Fed is trying to achieve in its fight against inflation. This places significant emphasis on today’s language from Powell.

Kansas City Federal Reserve President Ester George joined several other Fed board members in expressing hawkish views. She said that the Fed funds rate could be well over 4% but won’t know that until the Fed sees the data signs.

Chair Powell has been seen by the market as the least hawkish of Fed speakers of late. A change in tone from him could ignite volatility in many asset classes.

Reserve Bank of New Zealand (RBNZ) Governor Adrian Orr spoke to Bloomberg television after the New York close and gave a frank assessment of the quandary central bankers are facing.

He said that if central banks are doing their job in other parts of the world, then consecutive quarters of negative growth should be expected. He didn’t see that happening for New Zealand though.

Nonetheless, the Kiwi slid lower, dragging the Aussie and Loonie Dollars down with it and the US Dollar found support more broadly to varying degrees. Gold is steady near US$ 1,751 an ounce.

USD/JPY yawned at Tokyo CPI coming in above expectations for August. Year-on-year core CPI was 2.6% instead of 2.5% anticipated. The Tokyo CPI number provides insight into the national CPI figure that is due in 3-weeks’ time.

Crude oil slipped lower in the US session but has recovered some ground through Asia with the WTI futures contract near US$ 93.50 bbl, while the Brent contract is back above US$ 100 bbl.

The European benchmark Dutch Title Transfer Facility (TTF) natural gas futures contract has continued higher, trading above 320 Euro per Mega Watt hour (MWh) against the June low of 80 Euro per MWh. EUR/USD is little changed so far today.

APAC equities are all in the green and US equity futures are pointing to a flat start to the North American trading day.

Chinese stocks were underpinned by speculation that delisting risk in the US might be reduced. It is believed that Chinese companies will need to bring their accounts to Hong Kong where US regulators will review them.

While the PCE data out later today might gain some attention, the focus for markets will be on Fed Chair Jerome Powell’s speech at 1400 GMT today.

The full economic calendar can be viewed here.

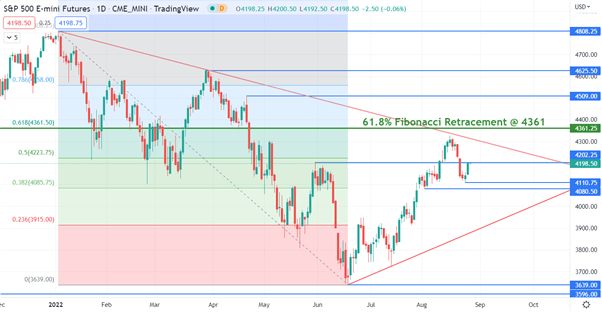

S&P 500 TECHNICAL ANALYSIS

The S&P 500 failed to break above a descending trend line last week and it may continue to offer resistance, currently near 4310.

Above it, the 61.8%Fibonacci Retracement of the move from 4808 down to 3639 could offer resistance at 4361.

On the downside, support might be at the recent lows of 4110 and 4080.

— Written by Daniel McCarthy, Strategist for DailyFX.com

To contact Daniel, use the comments section below or @DanMcCathyFX on Twitter

[ad_2]

Source link