[ad_1]

“You will lag the long-term average if your investment horizon misses the market’s few stellar years.”

Financial planners are on shaky ground when extrapolating the past into the future. Yet extrapolation underlies almost everything planners advise their clients to do. Stocks’ have beaten inflation by 6% annualized over the long term? Then build clients’ retirement financial plan on the assumption that this will be true for them too.

This is particularly dangerous advice at times like now when stocks are overvalued. It’s possible it will take decades for clients’ stock performance to live up to the assumed trend.

When I make this point to financial advisers, many think I’m referring to Japan’s stock market, since it trades today well below its all-time high in 1989, 34 years ago. They dismiss Japan’s experience as nothing more than an exception that proves the rule.

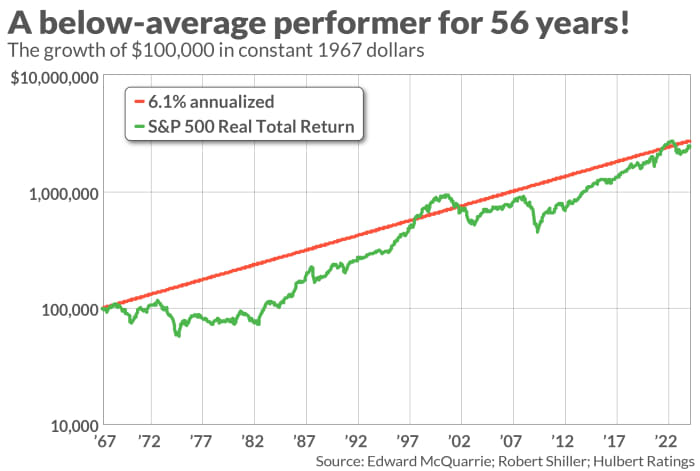

These advisers are shocked to learn that there have been even longer periods where the U.S. stock market was a below-average performer. In fact, this has been the case over the past 56 years, since September 1967. Though few are aware of this multi-decade stretch of below-average performance, the numbers don’t lie.

The stock market’s average real (inflation-adjusted) total return (dividend-adjusted) since 1793 has been 6.1% annualized, according to a database maintained by Edward McQuarrie, an emeritus professor at California’s Santa Clara University. This rate of return is represented by the red line in the accompanying chart.

In contrast, the green line represents the S&P 500’s

SPX

real total return since September 1967. On an annualized basis, its rate of return since September 1967 has been 5.7% annualized.

That may not seem a big difference, but it adds up. A $100,000 investment in stocks in September 1967 that grew at an annualized inflation-adjusted rate of 6.1% would today be worth $2.8 million in constant dollars. Invested in the S&P 500, that same $100,000 would instead be worth $2.3 million — a half million less.

You will notice from the chart that a September 1967 investment in the U.S. stock market rose above the 6.1% annualized trendline during the internet bubble years of the late 1990s, and then again (briefly) in 2022 before the bear market began in January 2023. It speaks to equities’ overvaluation in 1967 that it takes bubble-like performance to bring its post-1967 performance up to the long-term trendline — and only for so long as the bubble doesn’t break.

You may think this illustration has little relevance to today’s stock market, since the S&P 500’s real total return is 18% lower than where it was at the top of the bull market in January 2022. So even if bubble-like conditions existed then, you could still argue that much of the hot air has been let out of that bubble.

I’m not so sure this argument is persuasive. The S&P 500’s valuation in September 1967 was lower than now, even taking into account today’s stock market being 18% lower than it was almost two years ago. The S&P 500’s price/earnings ratio was 18.1 in September 1967, versus 18.9 today. Its cyclically-adjusted price/earnings ratio in September 1967 stood at 22.2, versus 28.6 today.

The takeaway, McQuarrie wrote in a recent email: “Stock market performance is lumpy and bunched, surging and languishing, for lengthy periods… [The stock market’s] “long term growth rate, even over two centuries, is biased upward by the few years in which the market soared.”

The investment implication: Even on the assumption the future is like the past, you will lag the long-term average if your investment horizon misses the market’s few stellar years.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at mark@hulbertratings.com

Plus: How to protect yourself from shady retirement advisers

[ad_2]

Source link