[ad_1]

S&P 500, VIX and Liquidity Conditions Talking Points:

- The Market Perspective: S&P 500 Choppy Range Between 3,910 and 3,650

- The final week of the year carries significant seasonal expectations for volatility and volume in the financial markets, but there is also an expectation for S&P 500 performance

- The 52nd week of the year averages a 0.5% gain from the S&P 500 back to 1900 and the VIX averages a drop to five month lows (‘summer doldrums) but there is a chance of for different outcomes

Recommended by John Kicklighter

Get Your Free Equities Forecast

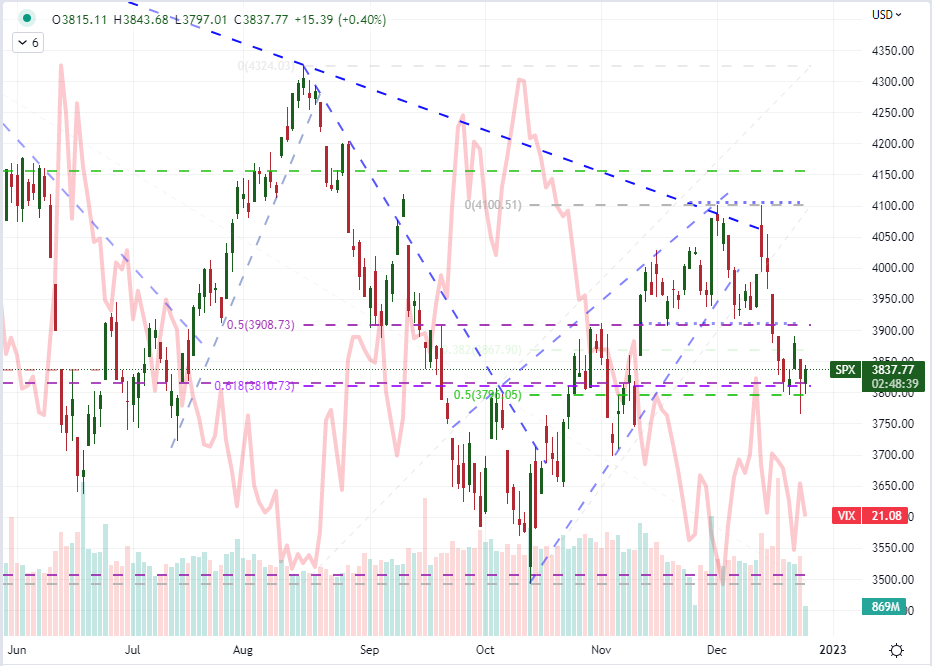

We are in twilight of liquidity for the 2022 trading year. Looking back on the ups and downs through the calendar year, it wouldn’t be controversial to say that the S&P 500 led risk benchmarks on a bearish trajectory. The technical ‘bear market’ designation (20 percent correction from all time highs), seven out of 12 months marking losses and the worst overall performance for a calendar year since 2008 are all viable criteria for just such an unflattering assessment. However, we have closed out the year just yet. There is one more week of trade left with heavy seasonal expectations competing with an unresolved backdrop for fundamentals with more than a few volatility surprise of late to draw upon a sense of skepticism. I prefer to move forward with expectations based on the practicalities of liquidity with a consideration of what that can do to volatility, momentum and direction. There is certainly a chance that we witness another bout of liquidity-amplified volatility before the year is drawn to a close and we evaluate January trade conditions. But always keep these developments in context.

Chart of S&P 500 with Volume Overlaid with VIX Volatility Index (Daily)

Chart Created on Tradingview Platform

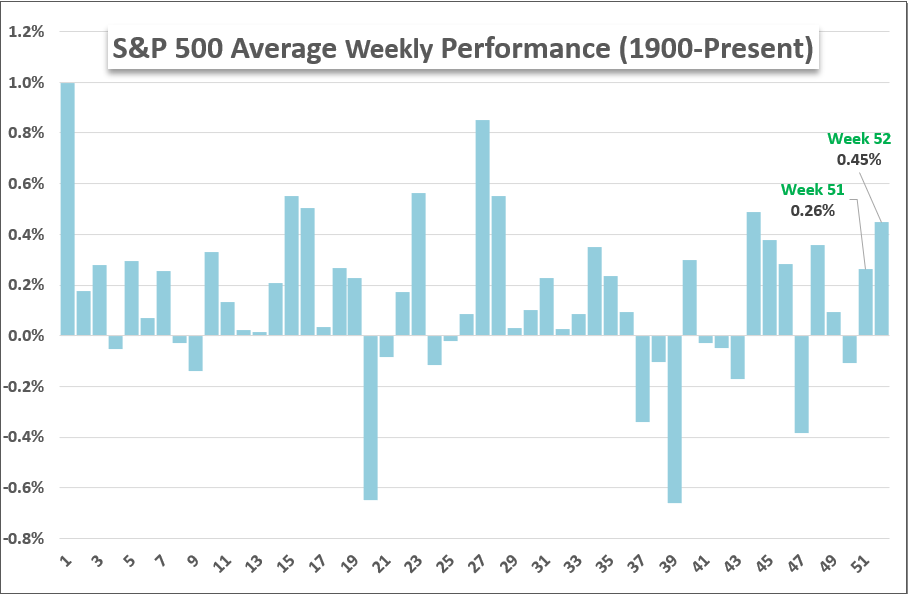

Looking to the historical averages, there is statistical weight to the popular seasonal designation of a ‘Santa Claus rally’. Averaging the S&P 500’s performance through each calendar week of the year back to 1900, the 52nd week has averaged a 0.45 percent gain. To immediately provide some practical skepticism to this outcome’s inevitability, consider that the 51st week of the year ahs averaged a 0.3 percent advance but the index ended up dropping -0.4 percent this past week. These are averages and they can take a wide range of performance metrics depending on the unique circumstances of each year. That said, the final week of the year is much more consistent when it comes to the drain of liquidity and a subsequent drop in overall volatility through that closing period.

Chart of S&P 500 Historical Average Performance by Week (Daily)

Chart Created by John Kicklighter

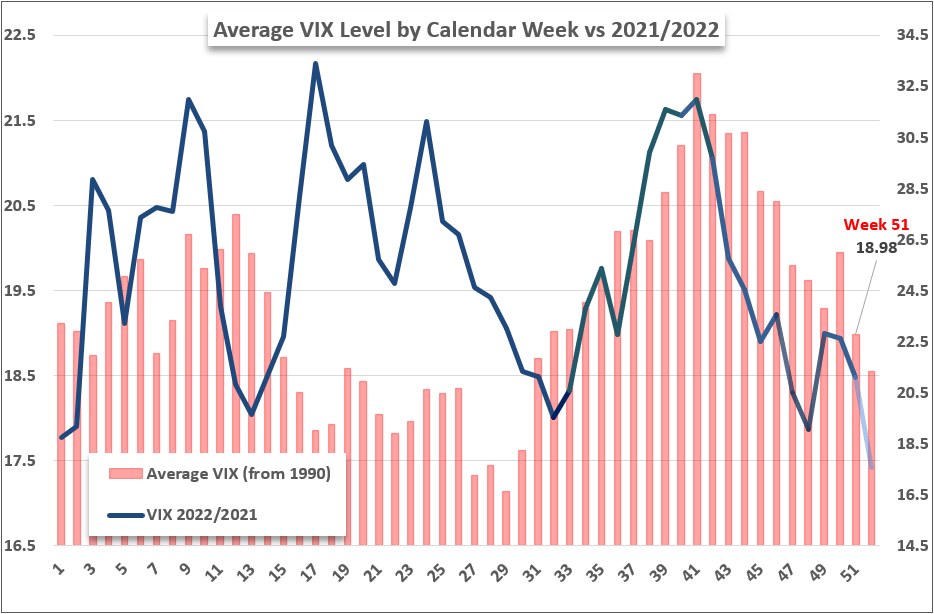

Looking to the historical norms of volatility via the VIX volatility index, this final stretch typically extends its slide from late Summer / early Fall peaks – and the statistical wobble that comes form the bout of indigestion through the 50th week of the year which usually houses the FOMC rate decision and a number of key economic reports. While the overall levels of the VIX this year have been somewhat off relative to the averages back to 1990, the general trend we have seen from these past three months have followed the pattern fairly well. If there is less market to trade and the docket is very thin (which it is), there is less potential for errant swells in volatility even when liquidity conditions could compound the market movement.

Chart of VIX Volatility Index Historical Average by Week Compared to 2022/2021 Actuals (Daily)

Chart Created by John Kicklighter

Statistics can sometimes be too abstract for people, so I wanted to take a look back to review two Decembers with very different overall performances relative to the seasonal averages for the month. December 2021 was largely in line with the typical performance for the month. The second to last week of the year last year generated a significant rally amplified by a preceding, sharp dip. With a very limited follow through on Monday of the 52nd, the final week would end in the green as well. Meanwhile, volume naturally deteriorated as the year came to a close and the VIX was happy to follow suit.

Chart of S&P 500 with Volume Overlaid with VIX Highlight December 2021 (Daily)

Chart Created on Tradingview Platform

The last significant deviation to the average December performance was back in 2018. What is normally a month that registers a gain, that year suffered a -9.2 percent loss – the biggest single month loss for the index all the way back to February 2009, at the close of the Great Financial Crisis. As significant as the overall month’s loss was, the final week of the year in 2018 was still a gain of approximately 2.9 percent. That is a significant advance that was likely amplified by the substantial tumble that preceded the rebound. While the middle of December this year has registered some significant ‘risk off’ it hasn’t been a one-way move that seems prone to normalization.

Chart of S&P 500 with Volume Overlaid with VIX Highlight December 2018 (Daily)

Chart Created on Tradingview Platform

Recommended by John Kicklighter

Get Your Free Top Trading Opportunities Forecast

[ad_2]

Source link