[ad_1]

S&P 500 OUTLOOK, FED SPEAK, CPI DATA, EARNINGS, UKRAINE WAR – TALKING POINTS

- S&P 500 outlook bearish ahead of volatile week of economic data and Fedspeak

- Earnings reports and escalation in the Russia-Ukraine war may amplify volatility

- SPX index hovering at 14-month low – technical analysis indicating soft rebound?

The S&P 500 may extend its decline as traders face another cascade of earnings reports and the publication of CPI data. Following the Fed rate decision, price growth indicators will continue to carry weight vis-a-vis the implications it carries for policy. However, from a technical perspective, it tells a cautiously, short-term optimistic story.

Having said that, with a precarious fundamental outlook against the backdrop of escalating developments between Russia and Ukraine – and the VIX market ‘fear gauge’ giving the highest reading since early March – the outlook for the S&P 500 in the week ahead looks increasingly bearish. Treasuries and the US Dollar may be the preferred asset traders reallocate their capital into.

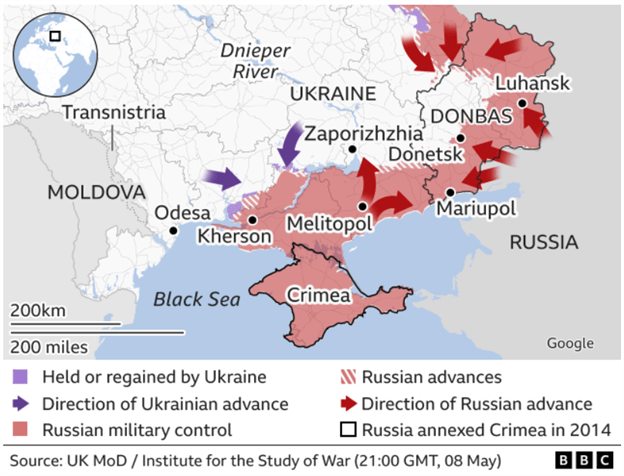

UKRAINE WAR UPDATE

The Ukraine war has entered its third month as Russian forces continue to secure the south with more eastern advances. Ukrainian soldiers in the Donbas region are holding for the time being while Russian troops are facing counterattacks around the city of Kharkiv. A few days ago, the town of Popasna was recently taken over and is now under Russian occupation.

Source: BBC News

The primary purpose of the southward-push is to secure the land corridor between Crimea and the “areas held by Russian-backed separatists in Donetsk and Luhansk”. The port city of Mariupol continues to draw international headlines and remains a thorn in the side of Russian forces who are encountering resistance inside the Azovstal steel plant.

For more updates on geopolitical risks, follow me on Twitter @ZabelinDimitri.

Meanwhile, back in Moscow, Russian President Vladimir Putin gave a speech during the country’s annual Victory Day parade, a celebration marking the triumph over Nazi Germany. Mr. Putin spoke about the national and sacred obligation to defend the motherland, pointing to the current fight in Ukraine being also about protecting Russian forces in Donbas.

He also mentioned NATO, referencing its expansion as a de-facto justification of Russian advancement into Ukraine as a preliminary strike against what some view as encroachment. As I noted in my previous report, Sweden and Finland are both now strongly considering formally joining the Western military alliance.

While that prospect could provide assurance to Western allies, it could inadvertently reinforce Putin’s claims that hostile forces are accelerating their encroachment on the Motherland. That credence could in turn fortify his rhetoric, potentially increasing support at home. However, there is another risk to consider if Sweden and Finland joined NATO.

Moscow has threatened a “military technical response”, putting the Nordic countries – and their neighbors – at risk of escalation. Markets have not immediately responded to the news, but a formal declaration could put investors on the defensive out of concern of what Russia’s response may be.

READ MORE: How to Trade the Impact of Politics on Global Financial Markets

US CPI DATA, FEDSPEAK

Traders will be eagerly waiting for the release of CPI and initial jobless claims data this week. Year-on-year price growth is expected to show an 8.1% print, slightly lower than the previous 8.4% reading. The latter is expected to rise to 192k, down from 200k. However, CPI data will carry more water in market terms following last week’s rate decision.

As expected, Fed Chairman Jerome Powell announced a 50-basis point rate hike to combat 40-year-highs in price growth: “The labor market is extremely tight and inflation is much too high”. Monetary authorities will have to balance slowing inflation while attempting to avoid a recession that tighter credit conditions could trigger.

Markets have felt the pain as they wean off an ultra-easy credit regime following the COVID-19 outbreak in March 2020. Consequently, with the focus on inflation, indicators such as CPI and Core PCE – the Fed’s favorite indicator – will almost certainly continue to be high-volatility events.

EARNINGS

Earnings from last week carried mixed results, with some such as Under Armour and Adidas suffering losses amid weak guidance and lockdowns in China (respectively). The former theme is likely one that will continue to appear as tighter credit conditions – and a potential economic slowdown from it – are expected to weaken profits in the coming months.

For the week ahead, investors will also see big-name firms such as Coinbase, Walt Disney, SoftBank, Sony, Honda, among many others announce their earnings. Reports across a wide array of sectors may induce cross-index volatility – e.g. industrial (Dow), tech (Nasdaq) – and potentially push investors out of equities into comparatively less-risky assets like the US Dollar.

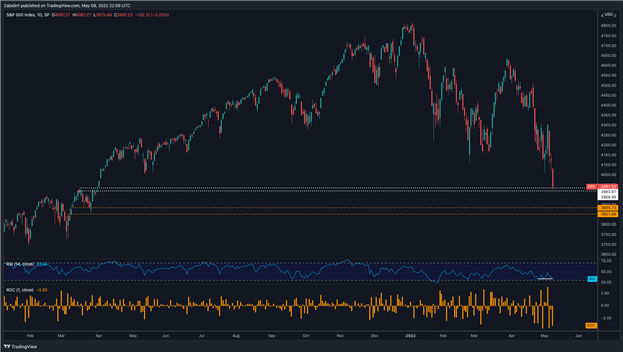

S&P 500 Outlook

The S&P 500 is down over four percent since last week, with Monday’s close stopping right on the upper crust of the former resistance-turned-support 3983-3968 band. It marked the biggest one-day decline since Thursday. If the decline continues, shattering the floor at 3968 could reinforce bearish sentiment and accelerate the S&P 500’s fall.

S&P 500 – Daily Chart

Chart created using TradingView

But is there a caveat? Yes. Positive RSI divergence indicates that downward momentum is slowing, and a reversal may soon ensue. However, as I have noted in my previous reports: technical indicators are tools to assess the relative risk-reward setup of a given asset at a particular time; it is not a prophecy.

Looking ahead, should sellers be overwhelmed by buyers looking to enter at a discount price, the S&P 500’s fall may temporarily be stopped. Having said that, the fundamental outlook for the week ahead, combined with gloomy technicals suggests any upward moves would be just that: a suspension, rather than a resolute reversal.

Written by Dimitri Zabelin for DailyFX

[ad_2]

Source link