[ad_1]

US Economy Moderates but Remains a Standout Amongst its Peers

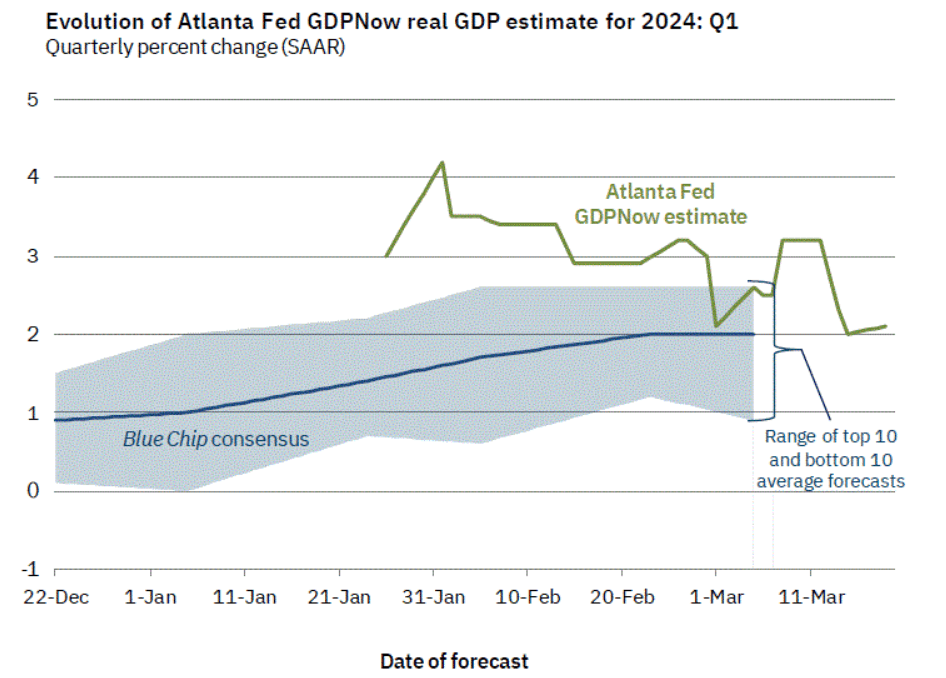

The US economy, according to the latest data from the Atlanta Fed’s GDP Now forecast, is projected to grow by 2.1% in Q1, after growing 3.2% in Q4 of 2023 and a massive 4.9% the quarter before that. While growth is clearly moderating, it remains stronger than other developed nations such as Europe, with is stagnant growth; and the UK which entered a technical recession in Q4. As such, the dollar is likely to remain supported into Q2 due to the potential for hotter activity and a robust labour market to add to existing inflationary pressures – which ultimately justify interest rates remaining ‘higher for longer’.

Graph 1: Atlanta Fed’s GDP Now Projection for Q1 Using Currently Available Data

Source: Federal Reserve Bank of Atlanta

Even Federal Reserve Bank officials were forced to confront the impressive level of growth as the March summary of economic projections included an upward revision for full year growth to reach 2.1%, up from 1.4% forecasted in December.

Robust Labour Market Necessitates Caution from the Fed

In the March Fed statement, officials agreed that risks to employment and inflation goals are moving into better balance, which can be viewed as optimism for a ‘soft landing’ – a situation where the Fed brings inflation down without sparking mass unemployment or a deep, long-lasting recession.

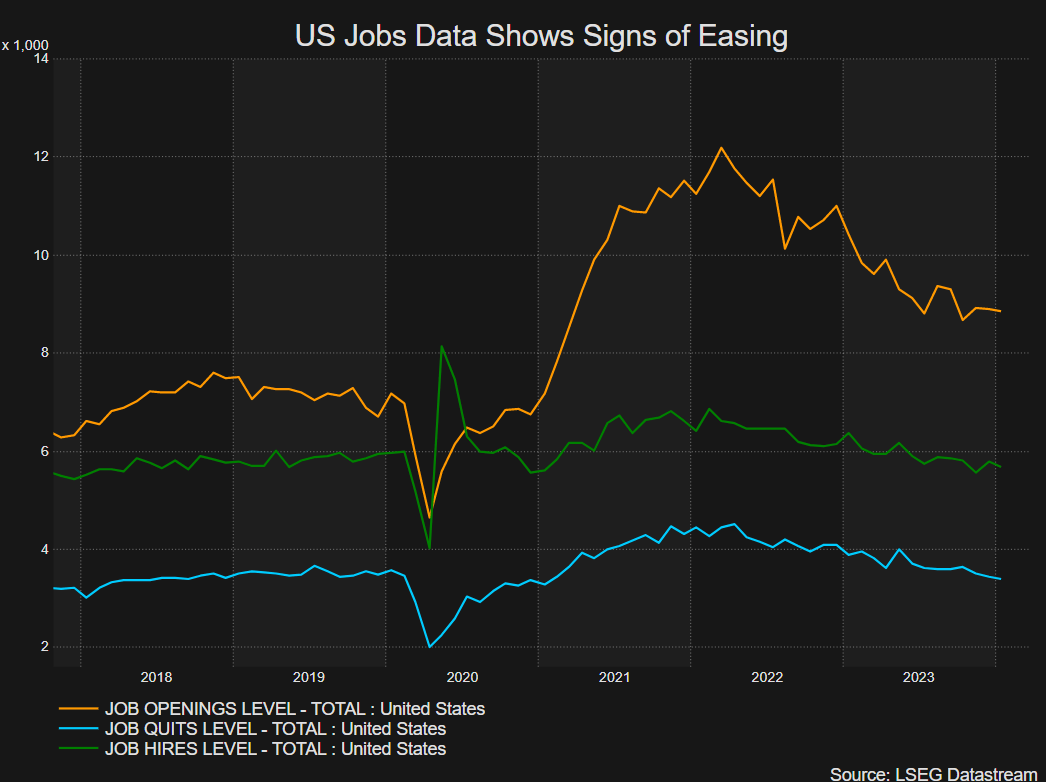

The Fed alluded to the overall resilience of the labour market by stating that job gains remain ‘strong’. January saw 229k jobs added while February contributed another 275k. However, signs of easing have appeared in the data that typically precedes larger declines in non-farm payroll data, and this is via the job opening and labour turnover (JOLTs) survey. There is a growing trend developing that sees fewer people quitting, fewer employers hiring and fewer available jobs, but the trend is in its infancy and hasn’t spilled over into actual jobs data. The longer this remains the case, the longer the Fed may have to hold out on rate cuts.

Graph 2: JOLTs Data Showing Job Openings, Quitting and Hiring

Source: Refinitiv DataStream, US Bureau of Labour Statistics (BLS)

After acquiring a thorough understanding of the fundamentals impacting USD in Q2, why not see what the technical setup suggests by downloading the full US Dollar Q2 forecast?

Recommended by Richard Snow

Get Your Free USD Forecast

The Fed Acknowledges Inevitable Rate Cuts but Timing Remains Uncertain

The upward revisions to both growth and inflation for 2024 sends a signal to the market that fundamentals remain strong and interest rate cuts will need to remain on the backburner until June or even July – according to current market implied expectations.

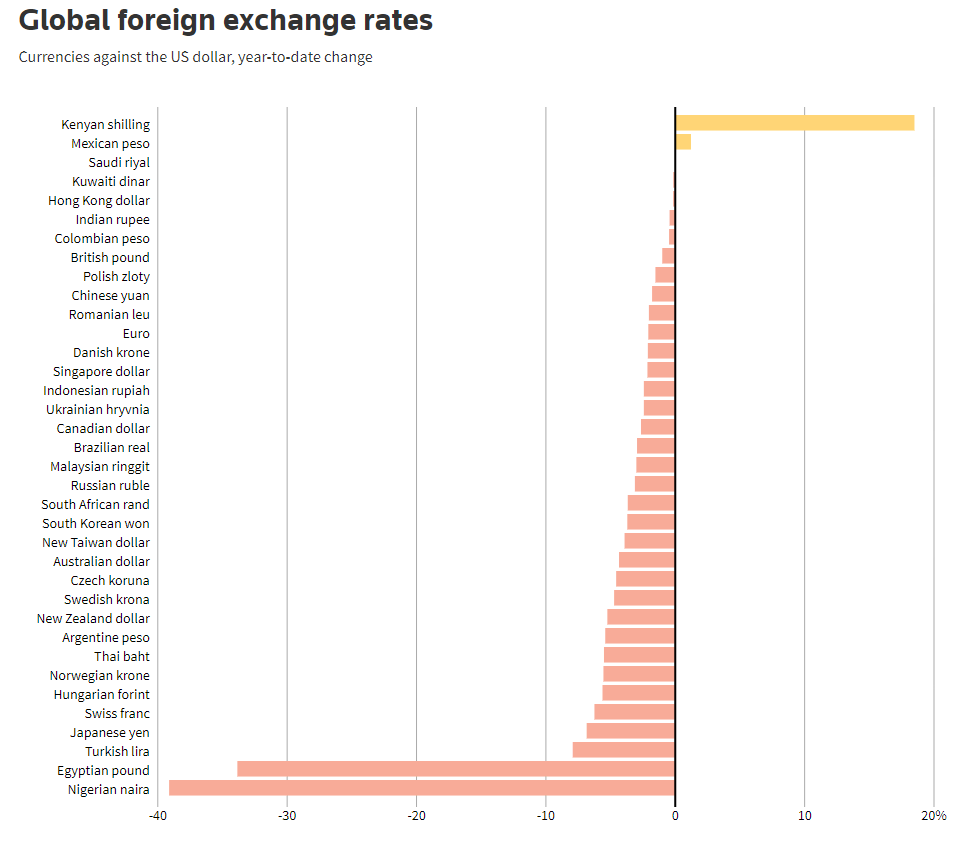

Other central banks, however, are not so fortunate. Several European Central Bank (ECB) officials, for example, have explicitly come out and identified June as a potential start date for rate cuts and will be hoping that the stagnant economy can hold on until then. Should incoming data sour even further, markets may start to price in an earlier hike or anticipate more than three cuts this year for the EU – which could weigh on EUR/USD. Since EUR/USD contributes more than 57% towards the US dollar basket (DXY), this is expected to support the benchmark of USD performance in Q2. The dollar has strengthened against most currencies this year (so far) and is likely to continue to benefit from a superior interest rate differential.

Global foreign exchange rates

Source: Thompson Reuters

Risks to the Bullish Outlook: Economy, Unemployment, and Inflation

Inflation has produced several hotter-than-expected prints in 2024 in some way or another which has led the Fed to dismiss any notion of imminent rate cuts. The risk in Q2 is that the hotter, seasonal factors buoying inflation, reverse. Rapidly declining inflation alongside robust jobs market significantly weakens the argument for maintaining rates at elevated levels.

In addition, the US economy is moderating – declining from annualised growth of 4.9% in Q3 to 3.2% in Q4 and on track for 2.1% in Q1 this year. Should signs of weakness appear, the Fed will be motivated to cut rates to avoid a recession. Employment is another factor that is keeping the economic machine humming. Job security and an abundance of available jobs has supported consumption and consumer spending to a large degree. A sharp decline in employment and news of increased layoffs pose a potential threat to the dollar in Q2, but current data remains strong.

Looking for actionable trading ideas? Download our top trading opportunities guide packed with insightful tips for the second quarter!

Recommended by Richard Snow

Get Your Free Top Trading Opportunities Forecast

[ad_2]

Source link