[ad_1]

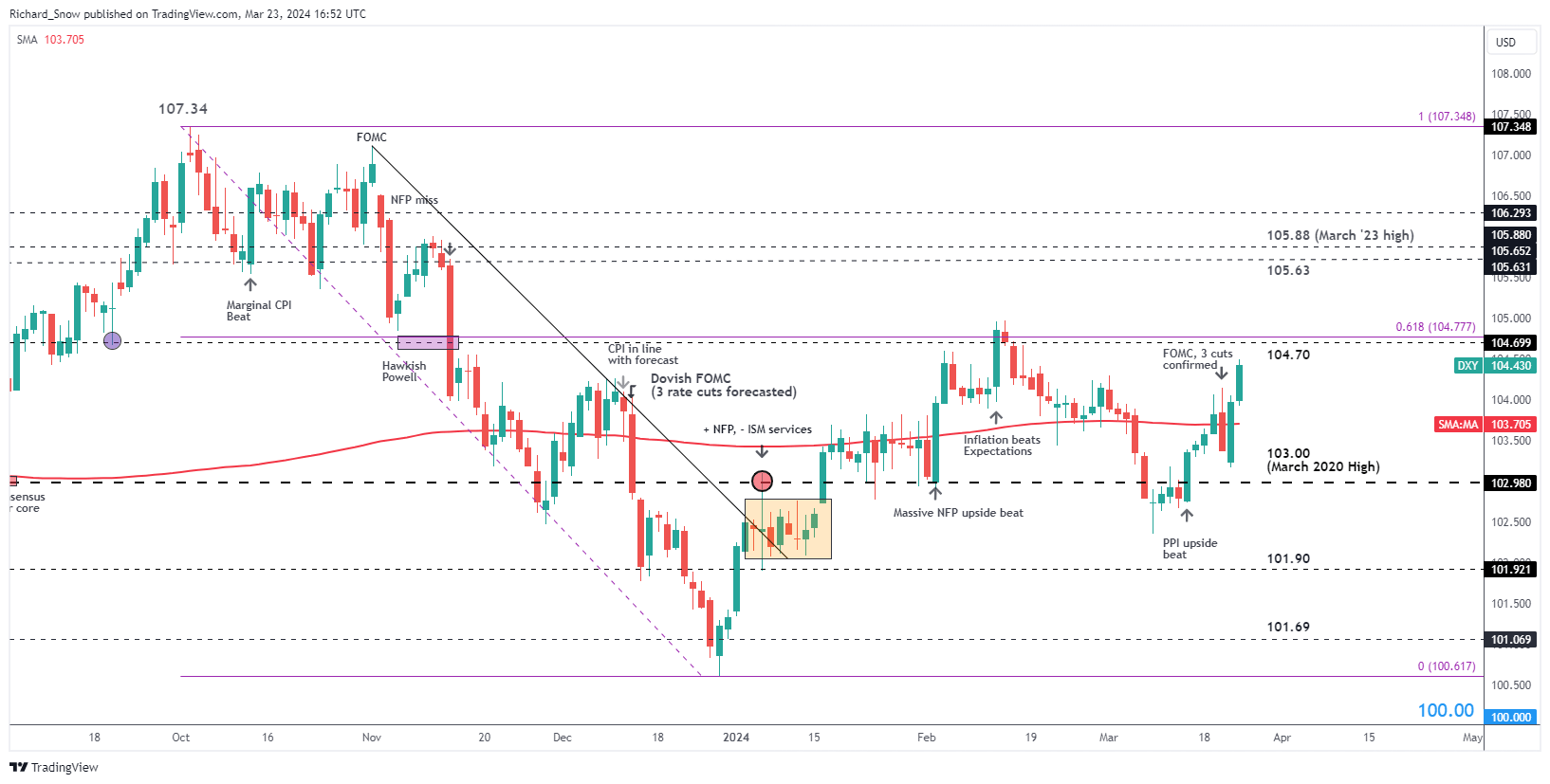

US Dollar Basket (DXY)

The generally accepted benchmark of US performance, the US dollar basket, has enjoyed a great start to the year. The dollar gained in strength as robust data reversed prior aggressive rate cut expectations. Price action received a late boost in March despite the Fed issuing a more dovish message and maintaining its projection of three rate cuts in 2024.

The index trades above the 200-day simple moving average towards 104.70 and the 61.8% Fibonacci retracement of the late 2023 selloff.

US Dollar Basket (DXY) Daily Chart

Source: TradingView, Prepared by Richard Snow

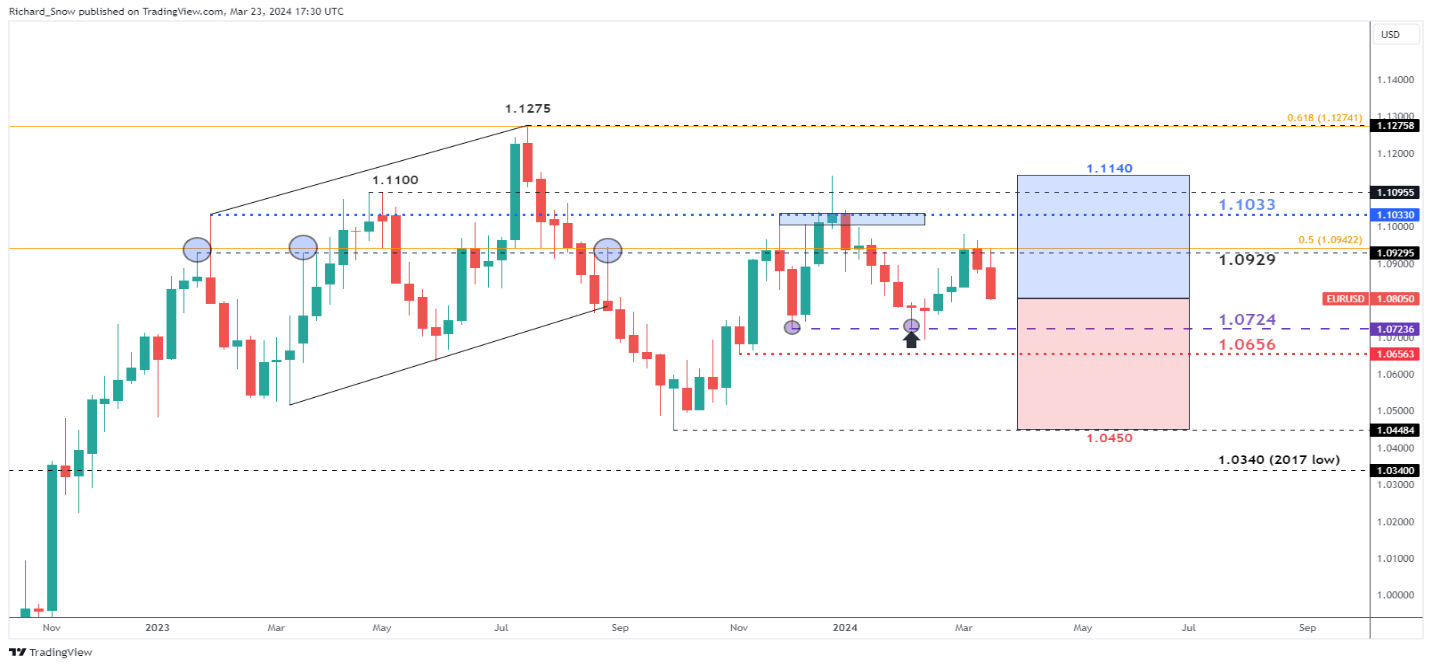

EUR/USD

EUR/USD weakened in Q1 as contrasting economic performance between the EU and the US developed further. In addition, the dollar benefits from a superior interest rate differential which tends to benefit higher-yielding currencies during periods of low volatility as investors seek to borrow lower yielding currencies to invest in higher yielders. This is more apparent in USD/JPY, but the same principle applies as the Euro tends to be overlooked by those seeking higher yielding currencies.

After finding resistance at 1.1033 and 1.1140, the pair was sent lower – finding support at 1.0724. Euro bulls attempted a comeback but fell short of retesting the yearly high and subsequently headed lower into the final few weeks of the quarter.

1.0724 remains a key level for EUR/USD in Q2 as it represents a tripwire for continued selling. The red and blue squares map out a rough range based on the average quarterly move taken from the last two quarters. Given the bearish euro and bullish dollar outlook, moves to the downside appear more prominently, with 1.0656 as the first target level and with 1.0450 highlighting a level consistent with a major selloff as well as the late 2023 swing low.

However, during this uncertain period where central banks aren’t sure when they will cut rates, forex moves will not be expected to move in a straight line. Therefore, levels of interest to the upside appear at 1.0929 followed by 1.1033 (prior resistance zone). Moves above 1.1100 towards 1.1140 would invalidate the bearish quarterly outlook.

EUR/USD Weekly Chart

Source: TradingView, Prepared by Richard Snow

After acquiring a thorough understanding of USD technical setups, why not find out what the fundamentals suggest for the second quarter buy downloading the full US Dollar Q2 forecast?

Recommended by Richard Snow

Get Your Free USD Forecast

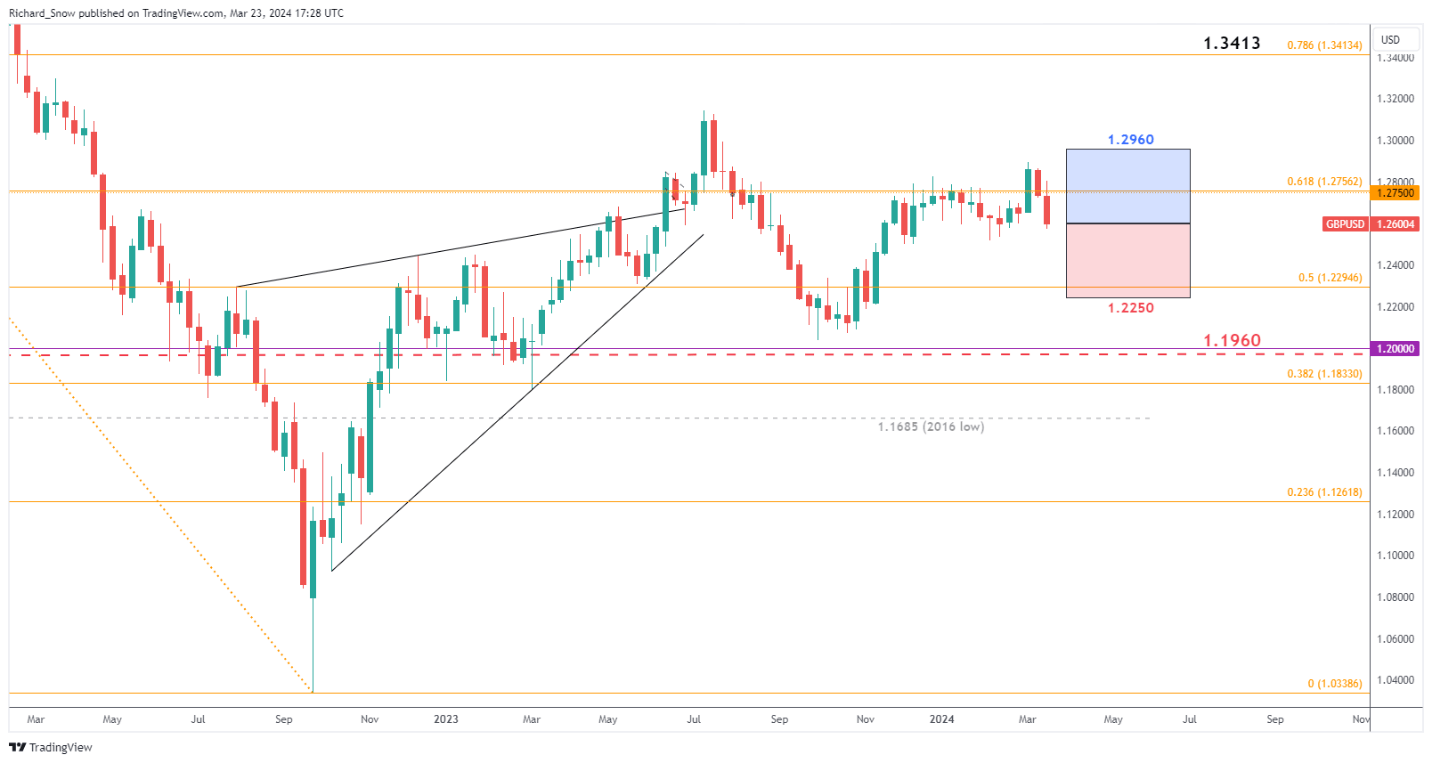

GBP/USD

The pound sterling is one of the better performers against the US dollar this year, barely registering a decline in Q1 after just having witnessed the post-NFP selloff. Hence, the outlook for GBP/USD is less bearish than for other major currencies. The Bank of England (BoE) positioned itself at the back of the pack when it comes to interest rate cuts, having struggled with persistently high inflation. This helped keep the pound supported. However, the February forecasts from the Bank anticipated inflation will sink to 2% by mid-year, bringing its rate cut path more in line with that of the US and EU.

Sterling has held up well against the high-flying greenback, boasting a bank rate of 5.25% which coincides with the lower band of the Fed funds rate (5.25% – 5.5%). On the weekly chart below, the same projection has been applied, mapping out potential upside and downside moves derived from the average move over the last two quarters.

To the downside, the initial hurdle to overcome is the 1.2520 level from the February swing low. Should inflation quickly accelerate as projected, a path towards 1.2250 opens, with 1.2295 (50% Fib level of the major 2021 – 2022 decline) a possible level of consideration ahead of it.

Upside levels of note include the 61.8% Fib retracement at 1.2756, followed by the 1.2960 marker which would invalidate a bearish GBP/USD Outlook.

GBP/USD Weekly Chart

Source: TradingView, Prepared by Richard Snow

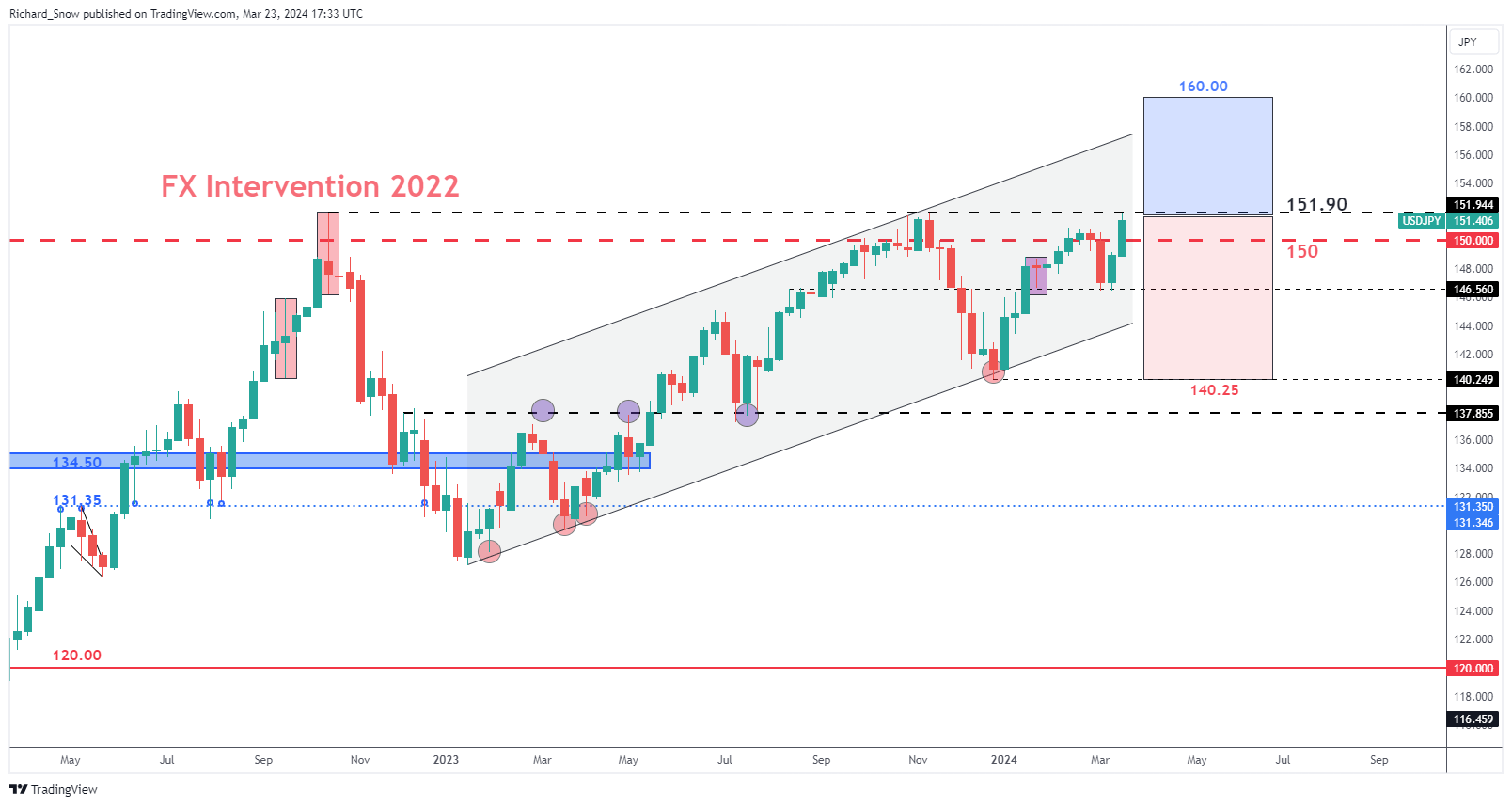

USD/JPY

USD/JPY has probably been the most publicised currency pair in Q1 due to the momentous decision from Bank of Japan (BoJ) officials to step away from negative interest rates. Signs of persistently high inflation coupled with the fastest rising wage growth witnessed over the last 30 years, emboldened the Bank to finally hike interest rates. However, the move did not strengthen the yen and actually saw a further deterioration in the value of the local currency. A struggling economy and difficult external environment limit the extent to which the Bank can add to existing hikes meaning the ‘carry trade unwind’ appears out of sight for now.

USD/JPY is a pair fraught with risk whenever it reaches, or surpasses, the 150.00 marker as the threat of FX intervention grows higher. Ministry of Finance representatives tend to voice their displeasure over the exchange rate whenever it is around the 150.00 level to quell bullish optimism.

Therefore, USD/JPY upside may be short-lived and remains a very risky trade above 150.00. Nevertheless, upside projections based off of quarterly moves for the last two quarters presents the ambitious topside move to 160.00 but, in reality, each 100 pips move above 150.00 appears more unlikely.

Lastly, a strong dollar limits the downside potential of the pair too, meaning in the absence of FX intervention from Tokyo, USD/JPY may favour more of a range around 146.56 and 152.00 in Q2. During the FOMC meeting, sources from Japan suggested the BoJ may hike once more, either in July or October but these fall outside of the forecast horizon for this report and may have a limited effect on the pair.

USD/JPY Weekly Chart

Source: TradingView, Prepared by Richard Snow

Looking for actionable trading ideas? Download our top trading opportunities guide packed with insightful tips for the second quarter!

Recommended by Richard Snow

Get Your Free Top Trading Opportunities Forecast

[ad_2]

Source link