[ad_1]

Investors are preparing for the release of a U.S. consumer-price index that may show no meaningful letup in inflation, leaving few safe places to hide just as systemic risks may be growing.

Coming just a few days after Silicon Valley Bank’s woes overshadowed Friday’s robust jobs report, the February consumer-price index report on Tuesday will put the focus squarely back on inflation.

Inflation traders expect to see a 6% year-over-year headline CPI rate for February, following January’s 6.4% reading and December’s 6.5% level. Even the narrower reading that strips out volatile food and energy costs may be a problem. Researchers at Barclays said the core reading should come in around 0.4% on a monthly basis and 5.5% year over year — little changed since January’s data.

That’s likely to add up to an environment in which investors will need to rely on less-traditional asset classes than ever before. When the U.S. suffered through stagflation in the 1970s, characterized by slow growth and persistent price gains, the most important takeaway for investors was that high inflation was uniformly bad across multiple countries for both stocks and bonds, which had a harder time generating positive real or inflation-adjusted returns, according to Deutsche Bank researchers Henry Allen and Jim Reid.

Meanwhile, regional-bank problems are further clouding the picture, by raising fears of systemic risks at a time when the Federal Reserve has turned more resolute about raising interest rates.

Many market participants are clinging to the hope of a less aggressive Fed rate hike on March 22 and policy path for the rest of the year. Meanwhile, the counterargument is being made that the central bank won’t be dissuaded by the sound of something breaking — a colloquial characterization of any damage done by the Fed’s full year of rate hikes.

Read: 10 banks that may face trouble in the wake of the SVB Financial Group debacle

Silicon Valley Bank’s problems “complicate things by making it really hard to get a read on financial conditions and by making a policy error more likely,” said Derek Tang, an economist at Monetary Policy Analytics in Washington. Still, “Fed policy makers are not in a position to pre-empt a financial crisis when inflation is so high. They just don’t have that luxury.”

See: Silicon Valley Bank is a reminder that ‘things tend to break’ when Fed hikes rates

While the impact of the past year’s rate hikes should already be working through the U.S. economy, Tang said via phone, “the other part of the story is that maybe the rate hikes so far are not enough to go against what is stronger, more-lasting inflation.” If the U.S. is indeed caught in a 1970s-style era of stagflation, cash and commodities, such as iron used in construction, would be among the most desirable assets for investors to hold, he said.

What makes the prospect of another 6%-level CPI reading so nerve-racking is the fresh uncertainty it could throw into financial markets over where the Fed needs to go with interest rates. Though policy makers prefer the PCE index and less-volatile core readings, the annual headline CPI rate matters because of its impact on household expectations. It’s been consistently above 6% since October 2021, though down from its peak of 9.1% last June.

Theoretically, another 6%-level annual headline CPI reading has the potential to boost the likelihood of a 50-basis-point Fed rate hike on March 22. It could also lead traders to price in a greater likelihood that rates will peak around 6% in 2023 and borrowing costs will need to stay elevated for one to two years.

According to Thomas Mathews, senior markets economist at Capital Economics, the Fed wants to avoid a repeat of the “stop-go” monetary-policy approach it took in the 1970s, when the central bank switch repeatedly switched between tightening and loosening financial conditions.

Back in the 1970s, the S&P 500

SPX,

produced an average nominal return of 6% on an annualized basis for the whole decade, though the index was down by 1% a year in real terms, according to Deutsche Bank. Treasurys “suffered too,” with nominal returns also wiped out by inflation, said researchers Allen and Reid, who described the decade as one of the worst ever for major assets.

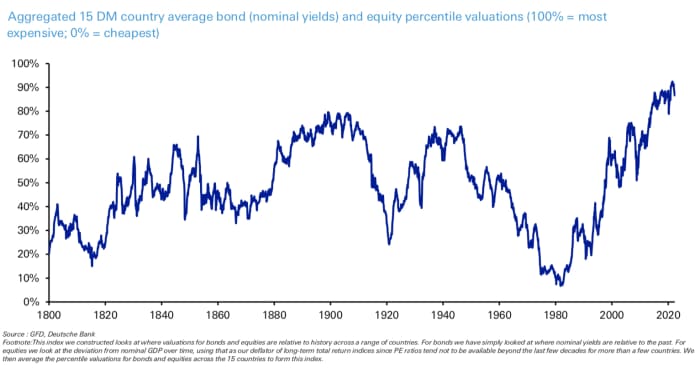

One index produced by the bank, which looks at more than a dozen developed-market bond and equity percentile valuations, reached its lowest level since 1800 by the end of the 1970s.

Source: Deutsche Bank

Over the past week, financial markets have toggled back and forth between pricing in the prospects of higher interest rates — reinforced by two days of testimony by Federal Reserve Chairman Jerome Powell — and gauging the damage caused by the central bank’s hikes thus far. The closure of Silicon Valley Bank has put a focus on the toll of higher rates, and placed a cloud over other banks.

On Friday, the policy-sensitive 2-year Treasury rate

TMUBMUSD02Y,

had its biggest one-day drop since 2008 as investors flocked to the safety of government debt. Traders boosted the likelihood of a less-aggressive, quarter-point rate hike later this month — which would take the fed-funds rate target to between 4.75% and 5%, from a current level of 4.5% and 4.75%. All three major U.S. stock indexes

DJIA,

COMP,

finished lower and posted their worst week of 2023.

Tuesday’s CPI report for February is perhaps the most important data for the week ahead. No major data is scheduled for Monday. On Tuesday, the NFIB Small Business Optimism Index is due ahead of the CPI report.

Check out: MarketWatch Economic Calendar

The February producer-price index is due on Wednesday, along with data on retail sales, the New York Fed’s Empire State manufacturing survey, and U.S. home builders’ confidence.

Thursday’s data releases are made up of weekly jobless claims, housing starts, building permits, and the Philadelphia Fed’s manufacturing survey. On Friday, updates roll in on industrial production, capacity utilization, the Conference Board’s U.S. Leading Economic Index, and the University of Michigan’s consumer-sentiment index.

[ad_2]

Source link